Big news for current and aspiring aircraft owners! On July 4th, 2025, the enactment of the “One Big Beautiful Bill Act” (OBBBA) ushered in a new era of pro-business tax incentives. For the aviation community, the most significant change is the permanent restoration of 100% bonus depreciation for qualifying property placed into service after January 19, 2025.

This isn't just a temporary boost; it's a fundamental shift designed to encourage businesses to invest. For those considering an aircraft acquisition, this change creates an unparalleled opportunity.

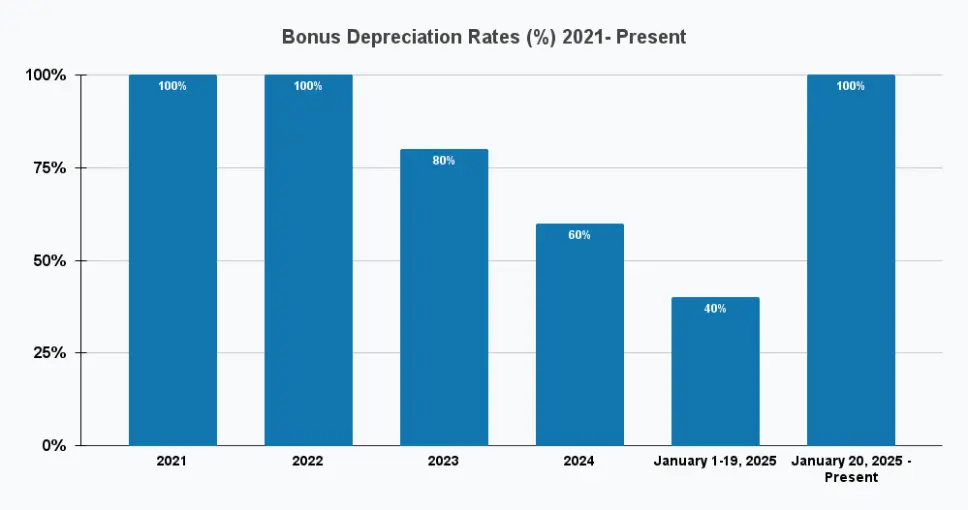

100% Bonus Depreciation is Back Permanently

Under prior law, bonus depreciation was on a scheduled phase-down (80% in 2023, 60% in 2024, and a mere 40% for the first part of 2025). The OBBBA has scrapped this phase-down entirely, reinstating the full 100% deduction.

- Key Dates to Note: To qualify for 100% bonus depreciation, your aircraft must be placed in service after January 19, 2025, and the binding contract to acquire it must have been signed on or after that same date. This timing distinction is crucial for maximizing your deduction.

This means businesses can now immediately deduct the entire cost of qualifying assets in the year they are placed into service, offering significant financial advantages.

What This Means for Aircraft Owners & Buyers

For aviation enthusiasts and businesses, this restoration is a game-changer. It allows for an immediate deduction of the entire cost of most aircraft, whether new or used, provided they meet the qualifying criteria.

- Qualifying Property: Generally, this includes tangible business property with a MACRS (Modified Accelerated Cost Recovery System) recovery period of 20 years or less. This broadly covers all business aircraft, including airframes, spare engines, and major components (typically 5 years for Part 91 operations, 7 years for Part 135/121). Used property also qualifies, as long as you haven't used it previously or acquired it from a related party.

- Section 179 Expensing: In addition to bonus depreciation, the OBBBA also raises the Section 179 expensing cap to $2.5 million for 2025 (phased out after $4 million in qualifying purchases). While bonus depreciation has no property cost limit and can create a net operating loss, Section 179 offers flexibility for partial expensing.

These provisions offer immediate tax savings, significantly reducing current year tax liability and enhancing cash flow for reinvestment or debt reduction.

Understanding Bonus Depreciation & Ownership Opportunities

Want to dive deeper into how these tax changes can directly impact your aircraft acquisition? Check out our video explaining the nuances of bonus depreciation, Section 179, and the various ownership opportunities available to you!

Navigating the "Business Use" Rules for Your Aircraft

To qualify for these powerful deductions, your aircraft must meet specific IRS standards for business use. This is particularly important for "listed property" like aircraft.

- Qualified Business Use (QBU): More than 50% of your aircraft's total hours, miles, or cycles must be devoted to a "qualified business use" in the year it's placed in service.

- Aircraft-Specific Test: For aircraft, a two-step standard applies:

- At least 25% of total hours must be from unrelated-party business use (e.g., third-party charters, customer demo flights, outside dry leases).

- Once the 25% threshold is met, the combined business and charter use must exceed 50%. Flights for owners or related parties only count after the initial 25% unrelated-party standard is met.

Maintaining detailed, contemporaneous records (logs including tail numbers, routes, dates, passengers, and business purposes) is essential to substantiate business use and avoid audit risks.

- Recapture Rules: If the QBU of your aircraft drops to 50% or below in a year after it was placed in service, you may need to recalculate depreciation and recapture any excess deduction as ordinary income.

- State Conformity: Be aware that many states (including California, New York, and Illinois) may not fully conform to these federal bonus depreciation rules, potentially requiring separate state tax calculations.

Why NOW is the Best Time to Invest in Aviation

The permanent restoration of 100% bonus depreciation under the OBBBA fundamentally changes the landscape for aircraft acquisition. The urgency to beat a phase-out is gone, but the strategic timing around contract dates and placed-in-service triggers remains vital.

This means:

- Immediate Cost Recovery: Deduct the entire cost of your qualifying aircraft in year one.

- Enhanced Cash Flow: Free up capital for other investments or business operations.

- Improved ROI: Accelerate the return on your capital project.

LifeStyle Aviation is uniquely positioned to help you capitalize on these new tax advantages. Our team of sales counselors understands the intricacies of aircraft ownership and the current market. We can guide you through selecting the right aircraft that not only meets your aviation goals but also aligns with these powerful tax incentives.

Ready to Make a Smart Investment?

Contact our expert team today to explore qualifying aircraft and discuss how these tax changes can benefit your specific acquisition strategy.